Is the 'r*' relevant for RBI?

A two-part post on India's monetary policy drivers and what to expect from the monetary easing cycle, that should kick off in October with a 25bp cut.

“In one word, the interest on money is, in reality, very often low when it seems to be high, and high when it seems to be low.”

-Wicksell, The Influence of the Rate of Interest on Prices, 1907

As the rate cutting cycle takes hold globally, there is a lively debate underway on where the policy rates will eventually settle. Central to this discussion is the natural rate of interest, or r*, which is the equilibrium real rate that neither stimulates nor depresses the economy. Put another way, it is the level of interest rate that prevails when the economy is operating most efficiently1 and inflation is stable.

Conceptually, real short-term rates should converge to r* over the long run as cyclical influences fade and structural forces dominate. This makes it a widely considered guidepost for monetary policy. If the current policy rate is below r*, then policy is accommodative, and vice-versa.

However, r* is not constant. It varies overtime, as its drivers2, such as trend growth rate, savings rate and government debt levels shift. The question currently on everyone’s mind is whether natural rates have moved higher post-pandemic3. If so, this may not only impinge on the quantum of the current easing cycle, but also keep policy rates above their pre-pandemic lows in the coming decades.

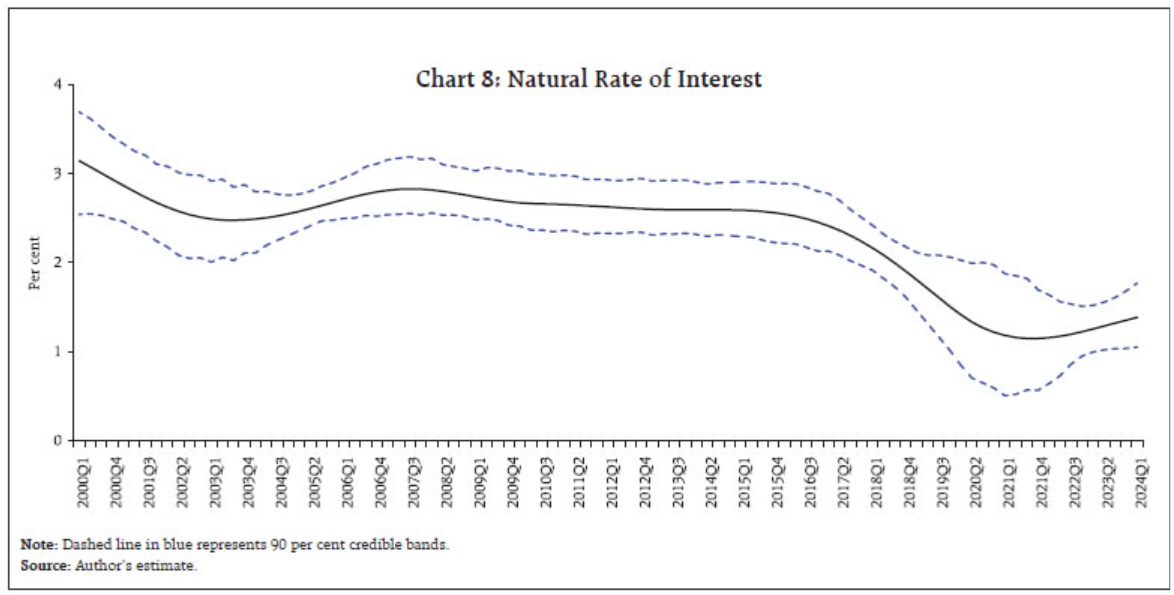

India is no exception. The RBI’s recently published estimates4 of India’s natural rate of interest, that indicate that the equilibrium interest rate has shifted back to pre-pandemic levels, have sparked a debate regarding the central bank’s easing intentions.

Updating the estimates of natural rate of interest for India with post-pandemic data, we find an upward shift, driven by growth of potential output. The estimate of the natural rate for Q4:2023-24 is at 1.4-1.9 per cent as compared with our earlier estimate of 0.8-1.0 per cent for Q3:2021-22. These estimates are centred in wide bands of uncertainty, warranting careful interpretation in the assessment of the monetary policy stance.

Governor Das has played down the estimates, noting that “neutral rate and all are theoretical, abstract concepts that cannot determine policy in the real world”. He is not entirely wrong.

Data issues magnify India’s r* estimation challenges

The unobservable nature of r* means that consensus on its level, or even direction, is hard to achieve. This is because the various approaches used to estimate the rate depend on assumptions about the long-term path of the economy, which itself are subject to considerable amount of uncertainty.

New York Fed President, John C. Williams, who co-created the widely used Laubach-Williams model to estimate r*, began a speech this July with…

For over 125 years, economists have grappled with a dilemma: How can a concept at the very heart of monetary theory be so vexing to quantify? I’m talking, of course, about r-star, the natural rate of interest.

He went on to note that while the natural rate cannot be wished away…

….the high degree of uncertainty about r-star means that one should not overly rely on estimates of r-star in determining the appropriate setting of monetary policy at a given point of time. Instead, such determinations must be, and are, based on a wide range of information and assessments, including those related to risks.

We think the challenges are greater in India’s case because the recurring concerns around the quality of economic data5, that feed into the measurement of unobservable variables like r*, increase the uncertainties. An official stock-taking of the country’s statistical releases is underway to improve data credibility. But for now, issues remain.