Macro Bite : War, Oil and Asia

Asia has enough stockpiles to weather at least a month of import disruptions. It'll still feel the impact of higher oil prices unless there is major de-escalation in the Middle East soon.

Energy prices had been trending up in the run up to the US-Israel strikes on Iran. With active hostilities now underway, the geopolitical premium has spiked. This is partly because the lack of clarity on the “very strong objectives” that the US has for invading Iran, and the speed with which the conflict is spreading across the Middle East, has made the endgame hard to ascertain.

For energy import-dependent Asia, this raises a spectre of supply disruption that could significantly impact energy availability and affordability — depending on the severity of the disruption and its duration.

On the first, the situation has already turned worrying.

Asia’s direct dependence on Iranian crude is limited, having fallen significantly since the withdrawal of the US from the nuclear deal in 2018 and the reimposition of sanctions on Tehran. True, China has sought to circumvent the sanctions through shadow fleets and transshipments. According to commodity intelligence firm Kpler, Iran accounted for 13.4% of China’s total seaborne crude imports in 2025. But there is little evidence of other Asian economies engaging in such practices to maintain meaningful commercial ties with Iran.

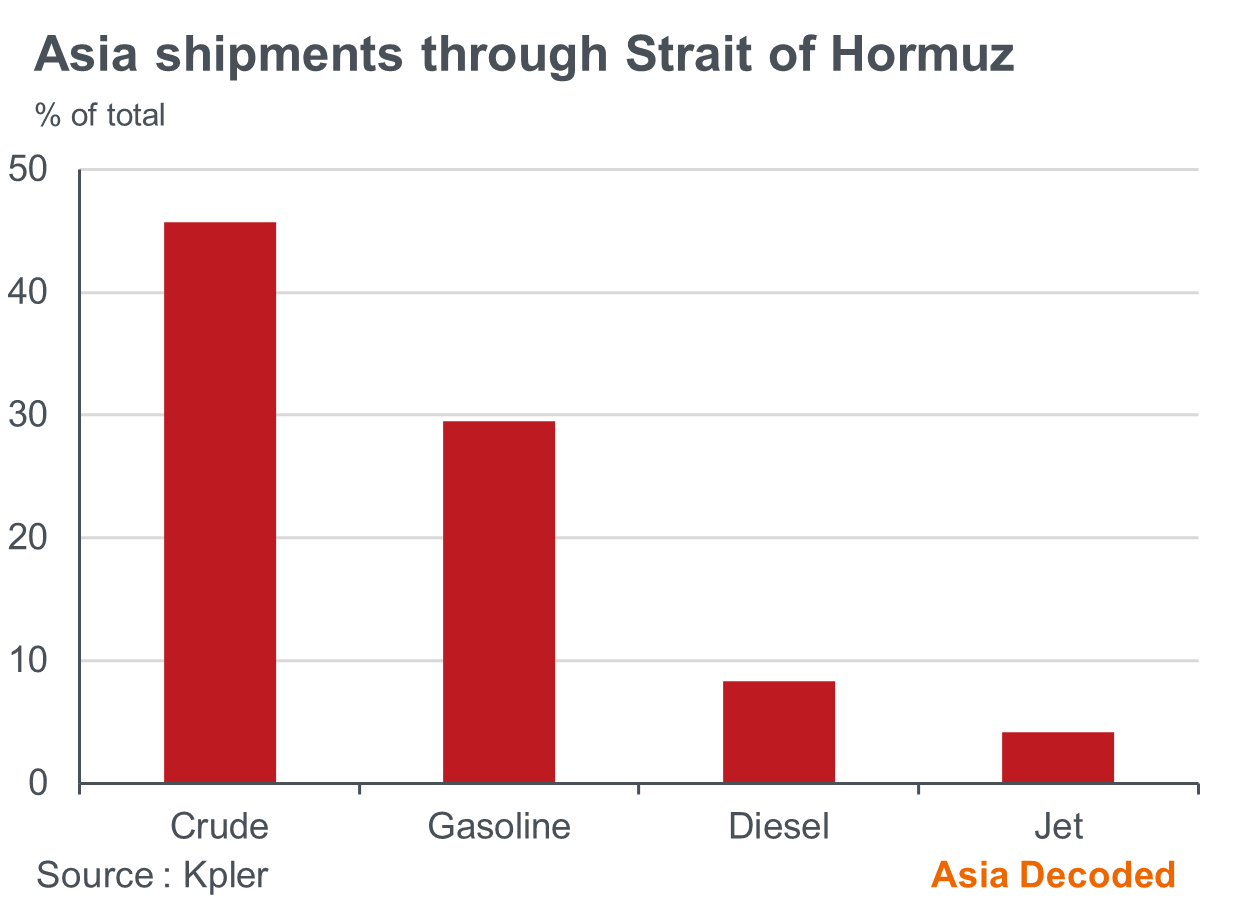

Still, this doesn’t insulate the broader region from supply shocks. At the heart of the matter is Iran’s stranglehold on the Strait of Hormuz, through which about one-fifth of the world’s oil and natural gas supply flows every day. It is also the primary route for energy shipments from the Middle East to Asia, and has come to a standstill amid rising security risks, compounded by growing hesitance of insurers to provide war coverage to vessels passing through the Strait.

Reports of Iranian drones targeting energy facilities in Saudi and Qatar, forcing temporary shutdowns, have further escalated supply concerns.

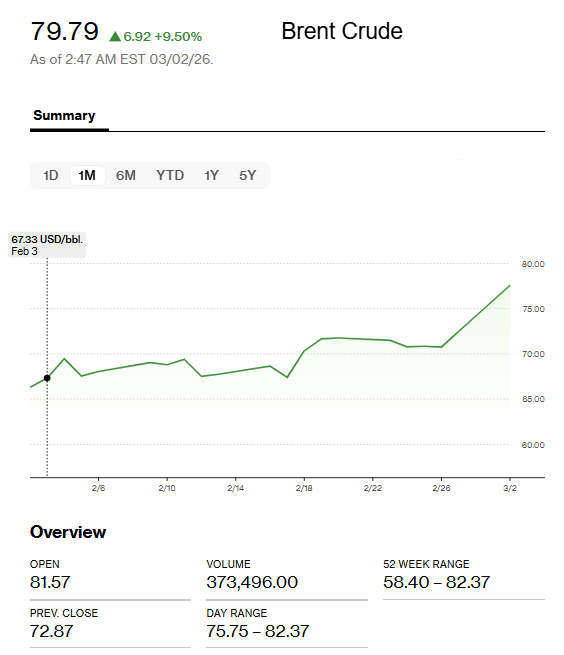

These developments are likely to keep energy prices under upward pressure until concerns about tightness in the physical market ease. At the time of writing, crude prices are up 8.8% from Friday’s close and trading just shy of $80/bbl.

It’s worth mentioning here that so far the problem is not the actual supply of oil, which most international agencies expected to comfortably exceed demand at the start of the year. The challenge is how that oil gets shipped to the destination if the main transit route is effectively closed.

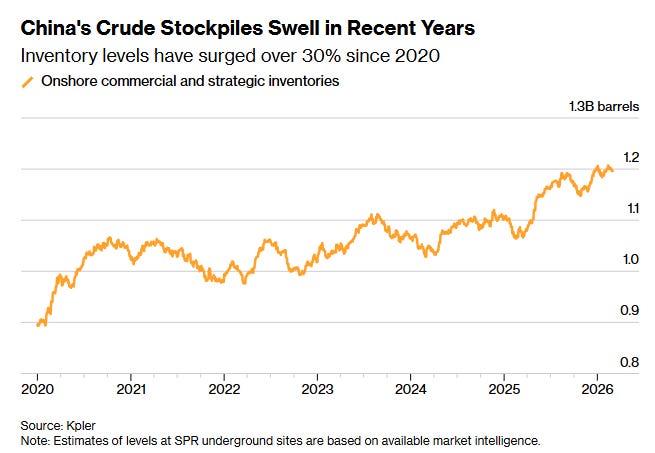

A prolonged disruption of the flows through the Strait of Hormuz would have substantial ramifications for Asia’s oil supply. But we don’t need to press the panic button yet. Newswires report that the region’s largest oil importers — China, India, S Korea, Japan and Thailand — have ample stockpiles to cover more than a month of imports, allaying concerns of immediate shortages.

That said, unless the war comes to an end in the next few days, the impact of higher oil prices will still be felt. It will likely hit Asian economies via rising import bills, deteriorating current account balances and weaker currencies, leaving aside the region’s two net energy exporters — Malaysia and Indonesia.

Whether this spills over into inflation meaningfully will depend on the persistence of price pressures and the extent to which governments choose to pass-through international prices to consumers. Even with declining subsidies in recent years, there is some scope for governments to lower excise duties, impose price ceilings and adjust administered prices to contain risks of runaway inflation. But they are likely to be constrained in their efforts relative to 2022 (Russia-Ukraine war) by elevated public debt levels.

The region’s largely inflation-targeting central banks are likely to prioritise inflation over growth. This doesn’t necessarily mean rapid rate hikes, which will depend on how inflation pans out. But the bar for further rate cuts will likely move higher.

On the whole, the Middle East war represents a downside risk to Asia’s growth for now, not a harbinger of an acute energy crisis. The situation, however, remains fluid and the risks are to the downside.

Stockpiles give a short-term buffer, but the Strait of Hormuz remains Asia’s structural chokepoint. Thanks for the reminder that energy security is ultimately about control over flows, not just reserves — a downstream vulnerability with upstream strategic implications for regional currencies, trade balances, and policy choices.